If you have found yourself asking what sticky inflation means, you are already past the headline level of the conversation. That is where things get more useful. Anyone can say inflation is “coming down” or “still too high.” The harder question is why some prices fall back quickly while others seem to ignore the memo.

That is the basic idea behind sticky inflation. Some parts of the economy adjust fast. Others move like they have all the time in the world. And unfortunately, the slow-moving parts often matter most for central banks, household budgets, and the broader outlook.

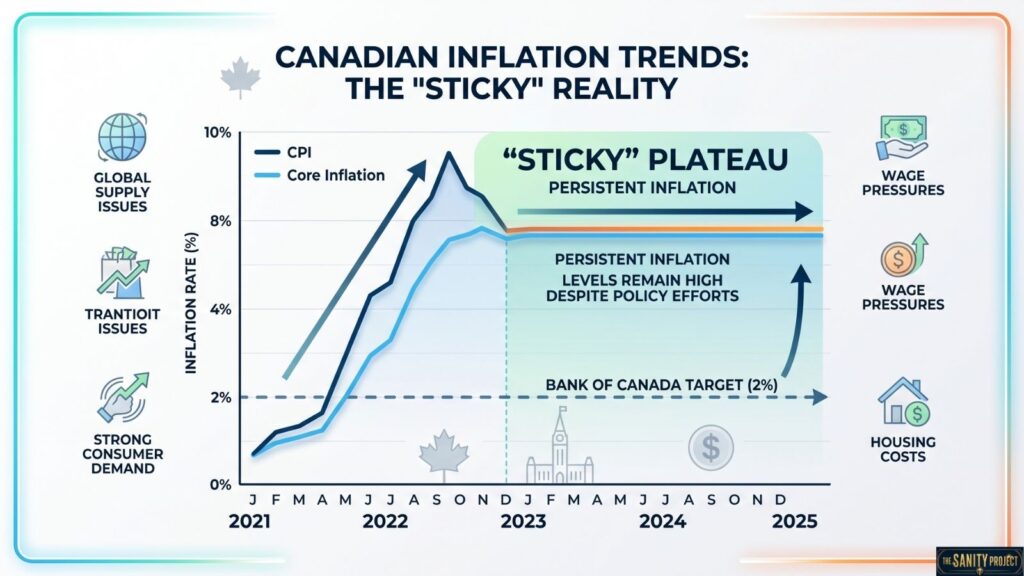

Quick Answer: Sticky inflation refers to a slow-to-decrease component of the consumer price index (CPI), where prices for goods and services remain elevated despite shifting economic conditions, such as falling demand or lower input costs. Unlike flexible prices, these “sticky” elements—often services like shelter and insurance—linger, hindering the return of overall inflation to central bank targets.

What does sticky inflation mean in plain English?

Sticky inflation refers to price increases that persist and do not decline easily, even after the original cause of inflation has started to fade. In other words, inflation becomes stubborn.

A one-time jump in gas prices is not usually what economists mean by sticky inflation. Energy prices can swing sharply in both directions. Sticky inflation shows up more in categories that tend to change slowly and then remain elevated, such as rent, wages, restaurant prices, insurance, medical services, and other service-heavy parts of the economy.

The key point is persistence. If inflation is sticky, prices are still rising persistently across certain categories, even when supply chains improve, shipping costs normalize, or commodity prices cool off. That is why policymakers worry about it. Temporary inflation is annoying. Sticky inflation is a policy problem.

Why are some prices “sticky”

Not all prices behave the same way, and pretending they do is what confuses people about inflation data.

Some prices are flexible. Gasoline, airline tickets, and some goods can move quickly in response to market conditions. If demand drops or supply improves, those prices can fall fairly fast. Other prices are stickier because they are tied to contracts, labour costs, regulations, or slow-moving negotiations.

Take rent. A landlord does not usually reprice apartments weekly due to changes in oil prices. Lease terms, local housing shortages, and broader wage trends shape rent over longer periods. The same logic applies to wages. Employers do not typically cut pay just because inflation reports look better for two months. Once wages rise, they tend to stay up. Businesses then build those higher labour costs into the prices they charge.

Services inflation is often the main culprit here. A haircut, a hospital visit, auto repair, legal advice, or child care depends heavily on labour. And labour costs tend to be sticky. Once they move higher, prices in those sectors often keep climbing or at least resist falling.

Subscribe To Our Newsletter!

So when economists talk about sticky inflation, they are often referring to the parts of inflation that are hardest to reverse because they are embedded in the structure of the economy, not just to temporary shocks.

What does sticky inflation mean for the Fed and rates?

For the Federal Reserve, sticky inflation means one uncomfortable thing: inflation may not go away on its own just because the obvious crisis has passed.

If inflation were caused only by clogged ports, chip shortages, or a sudden spike in oil, then time could do much of the cleanup. But if inflation has spread into wages and services, the Fed has a tougher job. It may need to keep interest rates higher for longer to slow demand and reduce pricing pressure.

This is why markets can get ahead of themselves. Investors see headline inflation cool and start betting on rate cuts. Then a sticky inflation measure comes in hotter than expected, and suddenly the “soft landing” consensus looks a little too neat. Reality tends to be less cooperative.

Central banks care about this because sticky inflation can shape expectations. If businesses expect costs to keep rising, they keep raising prices. If workers expect prices to keep rising, they demand higher pay. That feedback loop does not always spiral out of control, but it can make inflation much harder to fully bring down.

Sticky inflation vs headline inflation

This distinction matters more than most coverage suggests.

Headline inflation is the broad number you usually see in news reports. It includes everything in the basket, including volatile categories like food and energy. That makes it useful, but also noisy. A drop in gas prices can make inflation look much better, even while underlying pressure remains.

Sticky inflation tries to capture the categories that move more slowly and therefore tell us more about inflation’s staying power. Different indexes measure this in different ways, but the goal is the same: separate temporary price swings from more persistent trends.

This is also why core inflation gets so much attention. Core measures exclude food and energy, not because people do not buy food or gas, but because those prices can jump around enough to obscure the broader trend. Sticky inflation goes one step further. It focuses on prices that change slowly and, therefore, are more informative about long-run inflationary pressures.

So if headline inflation falls from 6 percent to 3 percent, that is good news. But if sticky inflation remains elevated, the all-clear signal may be premature. Not false, exactly. Just incomplete.

Where sticky inflation usually shows up

Housing is a classic example. Rent and owners’ equivalent rent move slowly, but they carry a lot of weight in inflation indexes. Even when market rents start to cool, official data can take time to reflect it.

Services are another major area. Think health care, education, hospitality, personal care, insurance, and repairs. These sectors depend less on imported goods and more on domestic wages and operating costs. That makes them less likely to snap back quickly.

Insurance has become a particularly useful example in recent years. Auto and home insurance costs have risen for reasons that are not easy to reverse quickly: higher repair costs, climate-related losses, reinsurance pressures, and more expensive vehicles. That is not a short-term blip. That is structural pressure showing up in a monthly data release.

Food away from home, meaning restaurant prices, is also often sticky. Once menus go up, they rarely come back down. Funny how that works.

Why sticky inflation matters to regular people

The phrase can sound abstract, but the effects are not. Sticky inflation is what makes households feel like official progress does not match lived experience.

You may hear that inflation is cooling, yet your rent is still higher, your insurance bill jumped again, and every service seems to cost more than it did a year ago. That gap between the macro story and the household story is often where public frustration comes from.

And to be fair, that frustration is rational. If prices rose sharply and then stopped rising as fast, people are still left with the higher price level. Slowing inflation is not the same as prices returning to their previous level. Sticky inflation reinforces that feeling because the categories that stay elevated are often the ones people pay for month after month.

For businesses, sticky inflation complicates planning. Borrowing costs may stay high. Wage expectations may remain elevated. Input costs may not normalize as quickly as hoped. It becomes harder to know whether higher prices are temporary enough to be absorbed or durable enough to be passed along.

Can sticky inflation go away without a recession?

Yes, but it is not automatic.

A labour market can cool gradually. Supply conditions can continue improving. Consumer demand can normalize without collapsing. Productivity can help offset wage pressure. All of that can ease sticky inflation over time.

But the path is narrow. If demand stays too strong, service inflation can remain elevated. If the labour market remains unusually tight, wage growth may continue to feed into price growth. If housing shortages persist, shelter inflation can stay sticky even with higher interest rates. There is no single switch to flip.

This is why inflation debates often sound more confident than they should. People want a clean answer: solved or unsolved, temporary or permanent, rate cuts now or later. The economy usually offers something less satisfying – a slower, messier adjustment.

What does sticky inflation mean for the bigger picture?

It means inflation is not just about shocks. It is also about how an economy absorbs those shocks.

When inflation becomes sticky, the issue is no longer only oil, ports, or pandemics. It is housing supply, labour market tightness, service-sector pricing power, and consumer behaviour. In other words, the deeper plumbing of the economy starts to matter more than the obvious trigger.

That is why sticky inflation deserves attention. It forces a better question than “Is inflation up or down?” It asks which prices are moving, why they are moving, and whether those moves are likely to last.

If you want a calmer way to read the inflation story, start there. Not with the loudest monthly number, and not with the most convenient narrative. Start with persistence. That is usually where the real signal is hiding.