A 5 percent raise sounds like progress right up until groceries, rent, insurance, and utilities climb by 6 percent. That is the basic problem with how inflation affects wage growth: pay can rise on paper while living standards quietly decline. People feel this instinctively, which is why public debates about wages often get oddly heated. The missing piece is usually not emotion. It is context.

Quick Answer: Inflation acts as a pressure valve on wages, typically forcing them upward as workers demand higher pay to maintain purchasing power. While inflation raises nominal wages (the amount paid), it often reduces real wages (purchasing power) if wage growth fails to keep pace with rising prices. High inflation often triggers a cycle of higher cost-of-living adjustments, leading to a “wage-price spiral” where rising costs and wages chase each other.

How inflation affects wage growth in the real world

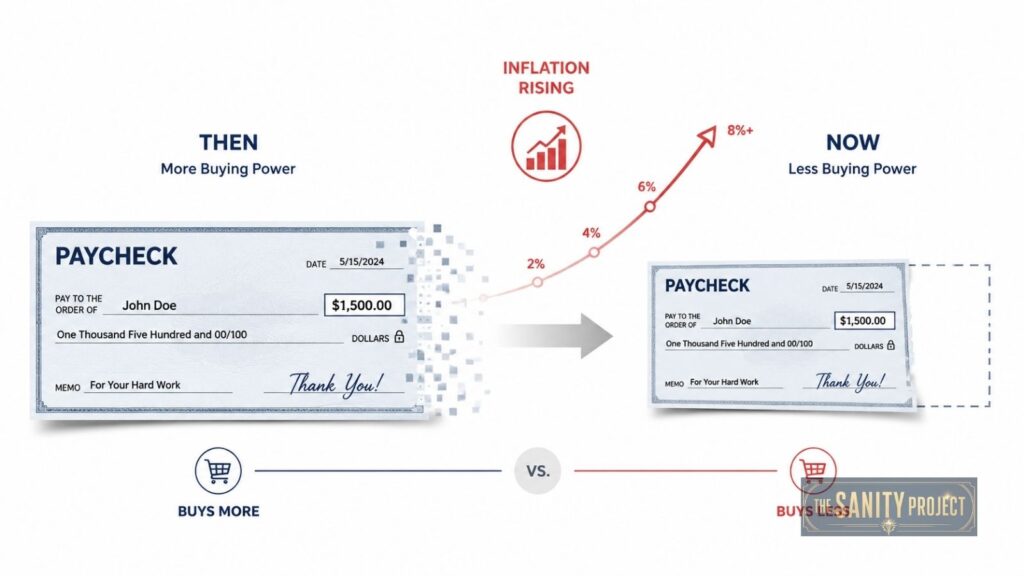

At the simplest level, inflation measures how quickly prices rise across the economy, while wage growth measures how quickly workers’ pay increases. The number that actually matters to households is real wage growth, which is wage growth after inflation.

If nominal wages rise by 4 percent and inflation runs at 2 percent, workers are generally better off. If wages rise by 4 percent and inflation runs at 5 percent, they are effectively losing ground. The paycheck is larger, but it buys less. This is where a lot of commentary goes off the rails. Bigger paychecks are not the same thing as better purchasing power.

That distinction matters because inflation does not just change prices. It changes the meaning of income. When commentators celebrate rising wages without asking what prices are doing, they are reporting only half the story – and often the less important half.

Why wages usually lag inflation

A common assumption is that if prices rise, wages should simply rise with them. If only labour markets were that tidy.

In practice, wages tend to adjust more slowly than prices. Businesses can raise prices within weeks or months, especially when input costs jump or demand stays strong. Wages, on the other hand, are often reset on a schedule. Annual reviews, union contracts, hiring cycles, and budget constraints all create delays.

That lag is one reason inflation feels so painful even when wage growth eventually catches up. For a period of time, workers absorb the shock first. Their rent goes up now. Their grocery bill goes up now. Their salary adjustment may not arrive until the next quarter, the next year, or not at all.

This is also why inflation can redistribute pain unevenly. Workers in sectors with strong bargaining power, high demand, or frequent job switching may see wages rise faster. Workers in lower-wage service jobs, fixed-salary roles, or weak labour markets often have less room to negotiate. Same inflation rate, very different outcomes.

Not all workers experience the same wage pressure

The phrase “workers” hides a lot of variation. Inflation does not hit everyone equally, and wage growth does not respond equally either.

Subscribe To Our Newsletter!

During tight labor markets, lower-wage workers sometimes see faster percentage wage gains because employers are competing to fill roles that are hard to staff. That happened in parts of the U.S. after the pandemic, when service employers had to raise pay to attract labour. For a while, some workers at the bottom of the pay scale saw stronger gains than many white-collar employees.

But there is a catch. Lower-income households also spend a larger share of their budgets on essentials such as housing, food, transportation, and energy. Those are often the categories that rise fastest during inflation spikes. So even when their wages grow faster in percentage terms, the relief may be thinner than headlines suggest.

Higher earners have more flexibility. They are more likely to own appreciating assets, hold jobs with stronger benefit structures, or have enough discretionary income to absorb rising costs. Inflation still affects them, but usually with less immediate strain. It is easier to tolerate a higher grocery bill when it is an annoyance rather than a budgeting event.

When wage growth helps – and when it feeds inflation

This is where the conversation usually gets lazy. People hear that wages are rising and assume one of two things: either workers are finally catching up, or wage increases are causing inflation. Both claims can be true in some cases. Neither is universally true.

If inflation begins because of supply shocks, energy costs, housing shortages, or sudden shifts in demand, wage growth may simply be a delayed response. Workers are trying to recover lost purchasing power, not create a new inflation cycle.

But if wages rise rapidly across the economy and businesses pass those labour costs into prices, that can contribute to ongoing inflation. Economists sometimes call this a wage-price spiral, though the phrase gets thrown around with more confidence than precision. True spirals exist, but they are not the automatic result of every pay increase. Sometimes wages are chasing inflation. Sometimes they are pushing it. Sometimes both are happening at once.

The key question is whether wage gains are being matched by productivity. If workers produce more value per hour, businesses can often pay more without raising prices as much. If productivity is flat and labour costs climb sharply, firms have fewer ways to absorb the increase. There is no villain here, despite the way public debate often tries to assign one. There is just arithmetic.

The role of expectations

Inflation is partly about psychology, which sounds suspiciously soft for an economic topic until you see how it works.

If workers expect prices to keep rising, they push harder for raises. If businesses expect higher labour and input costs, they raise prices sooner and more aggressively. If consumers expect everything to cost more next month, they may buy now, which can keep demand elevated. Expectations can reinforce the trend before the underlying conditions fully settle.

That is one reason central banks care so much about inflation expectations. The Federal Reserve is not only trying to slow current inflation. It aims to prevent high inflation from becoming the norm in wage negotiations and business planning. Once that happens, bringing inflation down gets harder and usually more painful.

Why “wages are up” can still feel false

You can show someone data proving average wages have increased and still get a deeply unimpressed stare. Fair enough.

Average wage growth can be misleading for several reasons. First, averages hide distribution. Strong gains for certain industries or income groups can make the overall picture look better than what many households experience.

Second, inflation baskets are averages too. Official inflation data may show moderation, while a household feels crushed by rent, child care, or insurance costs. If the costs rising fastest are the ones you cannot avoid, the idea that inflation is easing can sound almost decorative.

Third, people compare their finances not only to last month, but to where they expected to be. If wages rise after two years of losing purchasing power, the gain may feel more like a partial repair than progress. Technically, better is not always experienced as better.

How inflation affects wage growth policy debates

Policy arguments about wages and inflation often turn into fake binaries. Raise wages and risk inflation. Fight inflation and hurt workers. Reality is less theatrical.

Monetary policy can cool demand and reduce inflation, but it can also weaken hiring and wage growth. That is the trade-off. When the Fed raises interest rates, it aims to slow spending and borrowing enough to bring inflation under control. The downside is that weaker labour demand usually means less bargaining power for workers.

Fiscal policy matters too. Governments can support incomes directly, but if support is too broad during a supply-constrained period, it can add to price pressure. On the other hand, targeted policies that increase housing supply, labour force participation, infrastructure capacity, or productivity can ease inflation pressures over time without relying only on demand destruction. Less elegant slogan, better result.

This is why serious analysis has to distinguish between short-term relief and long-term stability. A policy that boosts paychecks today may help households immediately while making inflation harder to control. A policy that crushes inflation quickly may restore price stability while increasing unemployment. Neither side of that trade-off deserves a bumper sticker.

What to watch instead of the headline number

If you want a clearer view of how inflation affects wage growth, ignore the single headline claim and watch the relationship between three things: nominal wage growth, inflation, and productivity.

When wages are rising faster than inflation, households are gaining purchasing power. When inflation is outrunning wages, living standards are under pressure, no matter how upbeat the jobs report sounds. When productivity rises alongside wages, those gains are more likely to last. When it does not, inflation risks linger.

It also helps to ask who is benefiting. Are wage gains concentrated in a few sectors? Are lower-income workers catching up, or are they still getting squeezed by the cost of essentials? Is housing doing most of the damage? These questions are less catchy than “pay is up,” but they tell you more about whether the economy is actually improving for real people.

The broader lesson is simple. Inflation and wage growth are not opposing headlines. They are part of the same story. Looking at one without the other is how you end up feeling confused by an economy that looks fine in charts and expensive in real life.

A raise is only good news if it buys more than the last one did. That may not be a comforting answer, but it is at least an honest one.